China: drag on semiconductor market?

The Chinese stock market (as measured by the Hang Seng Index) dropped 11% from 14th August to 24th August over concerns of a slowing economy. In reaction, the U.S. stock market (as measured by the S&P 500) dropped 11% from 17th August to 25th August. The China market has since rebounded 2% while the U.S. market rebounded 5%. Will a slowing China drag down the global economy? China accounts for about half of the global semiconductor market. Will slowing semiconductor demand in China lead to a major slowdown in the global semiconductor market?

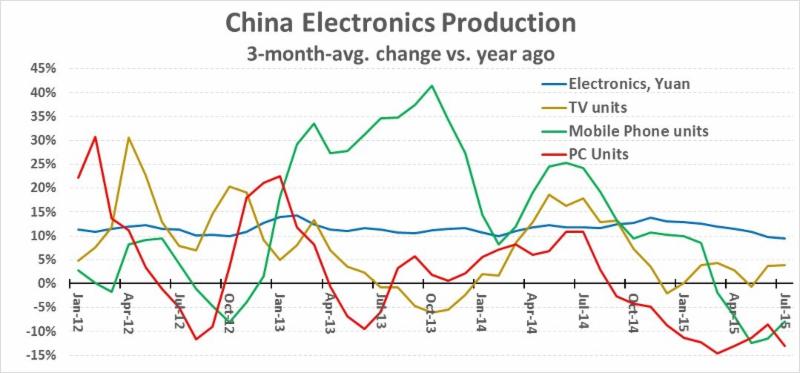

Chinese electronics production data presents a mixed picture as shown below. Unit production three-month-average change versus a year ago shows mobile phones went negative in March 2015. Mobile phones also went negative in 2012 before bouncing back to strong growth in 2013. PCs turned negative in September 2014, reflective of the weak global demand for PCs. Televisions were negative in December 2014 and May 2015, but have generally had modest growth in 2015. In contrast to the volatility of unit production, the overall change in electronics production as measured in Chinese yuan has been steadier. Overall electronics production growth has been below 10% for the last three months after averaging 12% for the years 2012 to 2014.

Over the last ten years, China GDP growth has been gradually slowing down. Following double-digit growth in 2006-2007, GDP dropped to 9.6% in 2008 and 9.2% in 2009, still strong growth especially since most of the rest of the world was experiencing a major recession. Growth picked back up to 10.4% in 2010 and moderated to 7.4% in 2014. The International Monetary Fund projects China GDP will continue to decelerate to 6.0% in 2017 before increasing to 6.3% in 2019 and 2020. China electronics production growth (as measure in yuan) has averaged 4 percentage points above GDP growth from 2006-2014. Our forecast at Semiconductor Intelligence (SC IQ) is electronics will grow in the 9% to 10% range through 2020.

Thus China should still be a major growth driver of the global economy and semiconductor market for at least the next few years. The behaviour of stock markets is almost impossible to predict and difficult to explain. Stock markets are influenced by economic factors, short term computer trading, greed and fear. We believe the recent behaviour of the China and U.S. stock markets are not a sign of a significant slowing of the growth of the Chinese economy in the next few years.

Featured products

MAX17793

Analog Devices Inc.

3V to 80V, 3A, High-Efficiency, Synchronous Step-Down DC-DC Converter

| SKU: | MAX17793 |

|---|---|

| Stock: | 9316 |

| Cost: | $3.64 |

MAX22516

Analog Devices Inc.

IO-Link Data Link Controller with Transceiver and Integrated DC-DC

| SKU: | MAX22516 |

|---|---|

| Stock: | 8000 |

| Cost: | $5.42 |