800V EVs charge into the mainstream using SiC power electronics

The demand for electric vehicle (EV) power electronics will increase dramatically in the next 10 years, primarily driven by rapid growth in the BEV car market, where IDTechEx predicts a 15% CAGR globally over the next decade.

Currently, the weighted-average battery capacity of BEV cars is increasing in all regions, piling pressure on battery supply chains, and creating uncertainty. The result is that drive cycle efficiency must come to the forefront of powertrain design, meaning the time has come for high voltage wide bandgap (WBG) power electronics.

The new IDTechEx report “Power Electronics for Electric Vehicles 2023-2033” provides a deep-dive into EV power electronics with technology insights into the evolving semiconductor and package materials, including Si, SiC and GaN semiconductors, die-attach materials, wire bonding, thermal management, and more.

IDTechEx presents granular forecasts detailing unit sales, GW and US$ demand for inverters, onboard chargers (OBC) and DC/DC converters segmented by voltage (600V, 1200V) and semiconductor type (Si, SiC, GaN).

While Si IGBTs have dominated the medium-to-high power device range for 20 years, including in EV power electronics, they are giving way to a new generation of WBG materials: SiC and GaN. This will fundamentally impact the design of new power devices, including the package materials, as high voltage and high power-density modules operating at higher temperatures becomes the trend.

The two drivers often cited to move from 350-400V to 800V and beyond are higher power levels of DC fast charging (DCFC), for example, 350kW, and drive cycle efficiency gains.

DCFC compatibility today is a relatively weak driver due to low availability versus AC chargers and the high costs associated with 800V infrastructure. Indeed, the IDTechEx report “Charging Infrastructure for Electric Vehicles and Fleets 2022-2032” estimates around 3 million AC charging installations took place in 2022, compared to ~50,000 DCFCs over 100kW. In addition, higher levels of DCFC does not necessarily drive a transition to 800V, although it is more optimal. Tesla is a good example, having deployed 250kW superchargers without moving beyond its 350V platform.

The efficiency argument for 800V is the stronger one. This allows joule losses to be reduced and high voltage cabling to be downsized. Combined with SiC MOSFETs, it typically leads to 5-10% efficiency gains, which can potentially downsize the expensive battery, save costs, or improve the vehicle’s range, creating a competitive advantage.

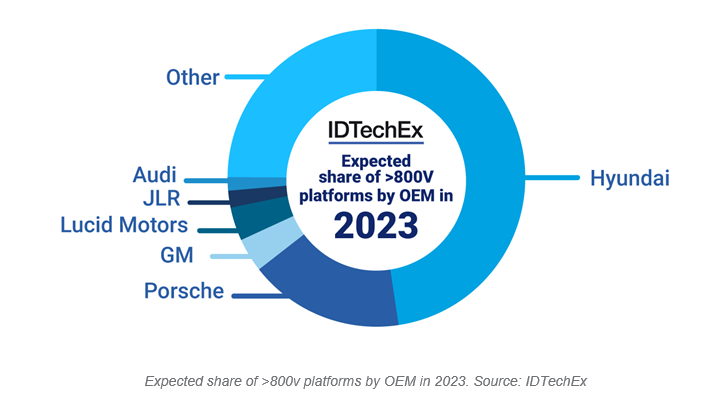

Yet, it is a challenging time for the automotive industry and 800V adoption experienced some pitfalls in 2022. The Lucid Air, the first 900V production car, sold around 7000 units in 2022 after an initial goal of 20,000. Porsche’s Taycan was also one of the OEM’s best-selling models in Europe between 2020 – 2021, but sales declined in 2022. Both are the results of continued parts shortages and supply chain challenges, for example, wire harness shortages with the Russia-Ukraine war.

On the other hand, Hyundai is demonstrating the success of 800V platforms. Sales of the company’s models using the 800V E-GMP platform more than doubled in South Korea to around 70,000 units/year, driven by the popularity of the IONIQ 5 and Kia EV6. This takes the 800V car market out of the luxury segment and predominantly into mainstream car segments for the first time. To support the rapid growth, Hyundai is diversifying its SiC supply partnerships, signing new deals with Onsemi and STMicroelectronics in 2022 to add to existing relationships with Infineon and Vitesco.

China is also signalling a transition to 800V vehicles, with development plans from major OEMs in 2022, including BYD, XPeng, Great Wall Motors, GAC, and others. These vehicles will most likely use SiC MOSFETs, allowing the SiC industry to tap into the world’s largest EV market, as China sold over 6.5 million EVs in 2022.

While 1200V SiC MOSFETs (adopted in 800V vehicle platforms) will play a key role in optimising drive cycle efficiency, it is still only one piece of the puzzle. Drive cycle efficiency can be improved in many areas, from improved battery chemistry to solar bodywork, high voltage cable reduction per vehicle, 600V SiC, improved motor design, and so on. The task for automakers is to work towards constantly improving the overall drive cycle efficiency to ensure battery supply does not go wanting.

Upcoming Free-to-Attend Webinar

Wide Bandgap Power Electronics: The New EV Battery

Luke Gear, Principal Technology Analyst at IDTechEx and author of this article, will be presenting a webinar on the topic on Thursday 30 March 2023 – Wide Bandgap Power Electronics: The New EV Battery.

This webinar will cover:

- Benchmarking of SiC versus GaN and future developments

- Materials evolution for power packages and industry pain points

- Market demand for SiC and opportunities for GaN

- A market outlook for EV power electronics broken down by voltage

To find out more and register a place on one of the three sessions, please click here

Featured products

MAX17793

Analog Devices Inc.

3V to 80V, 3A, High-Efficiency, Synchronous Step-Down DC-DC Converter

| SKU: | MAX17793 |

|---|---|

| Stock: | 9316 |

| Cost: | $3.64 |

MAX22516

Analog Devices Inc.

IO-Link Data Link Controller with Transceiver and Integrated DC-DC

| SKU: | MAX22516 |

|---|---|

| Stock: | 8000 |

| Cost: | $5.42 |

Product Spotlight

102991834

BeagleBoard

Single Board Computer (SBC), BeagleY-AI

AM67A BeagleY-AI Jacinto 7 AR...

| SKU: | 2820-102991834-ND |

|---|---|

| Stock: | 214 |

| Cost: | $56.24 |

SC1110

Raspberry Pi

Raspberry Pi 5 2GB

The Raspberry Pi 5 2GB model represents a leap for...

| SKU: | 2648-SC1110-ND |

|---|---|

| Stock: | 0 |

| Cost: | $38.33 |

AKX00069

Arduino

Arduino Plug and Make Kit

The Arduino Plug and Make Kit features the ...

| SKU: | |

|---|---|

| Stock: | 968 |

| Cost: | $66.97 |

300361-0011

Molex

MX150 Mid-Voltage MatSealed Female Connector Assembly, Dual Row, 20 Circ...

| SKU: | |

|---|---|

| Stock: | 280 |

| Cost: | $2.51 |