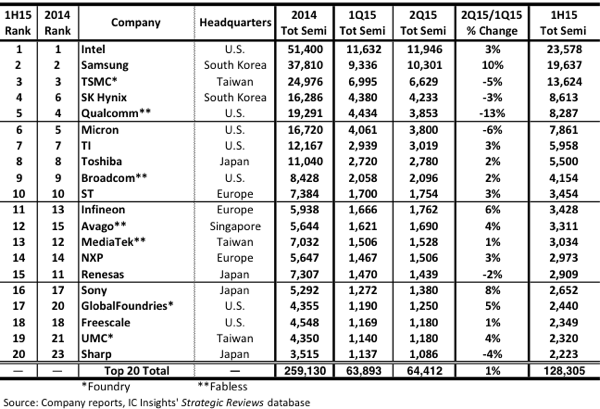

Top 20 semiconductor suppliers sales for 1H15

IC Insights will release its August Update to the 2015 McClean Report later this month. The August Update will include an in-depth analysis of the IC foundry market and a look at the top 25 1H15 semiconductor suppliers’ sales results and their outlooks for 3Q15 (the top 20 1H15 semiconductor suppliers are covered in this research bulletin).

The top 20 worldwide semiconductor (IC and O S D [optoelectronic, sensor, and discrete]) sales ranking for 1H15 is depicted in Figure 1. As shown, it took just over $2.2bn in sales just to make it into the 1H15 top 20 ranking and eight of the top 20 companies had 1H15 sales of at least $5.0bn. The ranking includes seven suppliers headquartered in the US, four in Japan, three in Taiwan, three in Europe, two in South Korea and one in Singapore. The top 20 supplier list includes three pure-play foundries (TSMC, GlobalFoundries and UMC) and four fabless companies.

IC Insights includes foundries in the top 20 semiconductor supplier ranking since it has always viewed the ranking as a top supplier list, not a marketshare ranking and realises that in some cases the semiconductor sales are double counted. With many of our clients being vendors to the semiconductor industry (supplying equipment, chemicals, gases, etc.), excluding large IC manufacturers like the foundries would leave significant 'holes' in the list of top semiconductor suppliers. As shown in the listing, the foundries and fabless companies are clearly identified. In the April Update to The McClean Report, marketshare rankings of IC suppliers by product type were presented and foundries were excluded from these listings.

It should be noted that not all foundry sales should be excluded when attempting to create marketshare data. For example, although Samsung had a large amount of foundry sales in 1H15, some of its foundry sales were to Apple and other electronic system suppliers. Since the electronic system suppliers do not resell these devices, counting these foundry sales as Samsung IC sales does not introduce double counting. Overall, the top 20 list in Figure 1 is provided as a guideline to identify which companies are the leading semiconductor suppliers, whether they are IDMs, fabless companies or foundries.

Figure 1 - 1H15 top 20 semiconductor sales leaders ($m, including foundries)

In total, the top 20 semiconductor companies’ sales increased by only 1% in 2Q15/1Q15, the same growth rate as the total worldwide semiconductor industry. Although the top 20 semiconductor companies registered a 1% sequential increase in 2Q15, there was a 23-point spread between Samsung, the fastest growing company on the list (10% growth), and Qualcomm, the worst performing supplier (13% decline) in the ranking. Moreover, given Qualcomm’s currently dismal guidance for 3Q15, the company is on pace to post a semiconductor sales decline of 20% in calendar year 2015.

Samsung’s excellent growth rate in 2Q15 put the company closer to catching Intel and becoming the world’s leading semiconductor supplier. In 2014, Intel’s semiconductor sales were 36% greater than Samsung’s. In 2Q15, the delta dropped by a whopping 20 percentage points to only 16%. However, with Intel providing guidance for a 3Q15/2Q15 sales increase of 8% and Samsung facing a lackluster DRAM market (primarily due to pricing pressures), additional gains toward the number one position may be difficult for Samsung to achieve in the near future.

There were two new entrants into the top 20 ranking in 1H15: Japan-based Sharp and Taiwan-based pure-play foundry UMC, which replaced US-based Nvidia and AMD. AMD had a particularly rough 2Q15 and saw its sales drop 35% year-over-year. In fact, in 2Q15, the company’s sales fell below $1.0bn for the first time since 3Q03, almost 12 years ago. It currently appears that AMD’s 2013 restructuring and new strategy programs to focus on non-PC end-use segments have yet to pay off (in addition to its sales decline, AMD lost $361m in 1H15 after losing $403m in 2014).

IC Insights has recently lowered its 2015 worldwide semiconductor market forecast from 5% to 2%. As was shown in Figure 1, the top 20 semiconductor suppliers in total had $128.3bn in sales in 1H15. This figure was just under 50% of the top 20 companies’ full year 2014 sales of $259.1bn. With only modest growth expected in the second half of this year for the worldwide semiconductor market, the top 20 semiconductor suppliers’ combined sales in 2015 are expected to be only about 1-2% greater than in 2014.

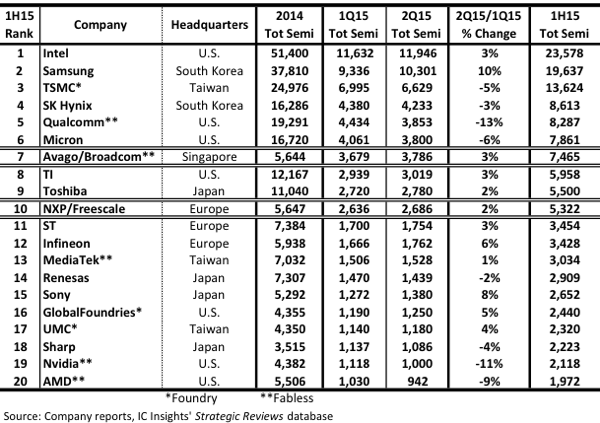

Figure 2 shows how the 1H15 top 20 ranking would have looked if the Avago/Broadcom and NXP/Freescale mergers were in place. As shown, Avago/Broadcom would have been ranked 7th and NXP/Freescale would have moved into the 10th spot. IC Insights believes that additional acquisitions and mergers over the next few years are likely to continue to shake up the future top 20 semiconductor company rankings.

Figure 2 - 1H15 top 20 semiconductor sales leaders after Avago/Broadcom and NXP/Freescale deals ($m)

Featured products

MAX17793

Analog Devices Inc.

3V to 80V, 3A, High-Efficiency, Synchronous Step-Down DC-DC Converter

| SKU: | MAX17793 |

|---|---|

| Stock: | 9316 |

| Cost: | $3.64 |

MAX22516

Analog Devices Inc.

IO-Link Data Link Controller with Transceiver and Integrated DC-DC

| SKU: | MAX22516 |

|---|---|

| Stock: | 8000 |

| Cost: | $5.42 |

Product Spotlight

102991834

BeagleBoard

Single Board Computer (SBC), BeagleY-AI

AM67A BeagleY-AI Jacinto 7 AR...

| SKU: | 2820-102991834-ND |

|---|---|

| Stock: | 208 |

| Cost: | $56.24 |

SC1110

Raspberry Pi

Raspberry Pi 5 2GB

The Raspberry Pi 5 2GB model represents a leap for...

| SKU: | 2648-SC1110-ND |

|---|---|

| Stock: | 0 |

| Cost: | $38.33 |

AKX00069

Arduino

Arduino Plug and Make Kit

The Arduino Plug and Make Kit features the ...

| SKU: | |

|---|---|

| Stock: | 968 |

| Cost: | $66.97 |

300361-0011

Molex

MX150 Mid-Voltage MatSealed Female Connector Assembly, Dual Row, 20 Circ...

| SKU: | |

|---|---|

| Stock: | 280 |

| Cost: | $2.51 |